💳Cannabis Payments Quick Guide 2025

- Carpfish Creative

- Sep 8, 2025

- 8 min read

The cannabis payment processing landscape in 2025 remains complex, with businesses operating in a regulatory gray area between federal prohibition and state legalization. While traditional credit card processing is still unavailable for direct cannabis sales, specialized payment processors have emerged to serve this high-risk industry with solutions including PIN debit, ACH transfers, and cashless ATM systems.

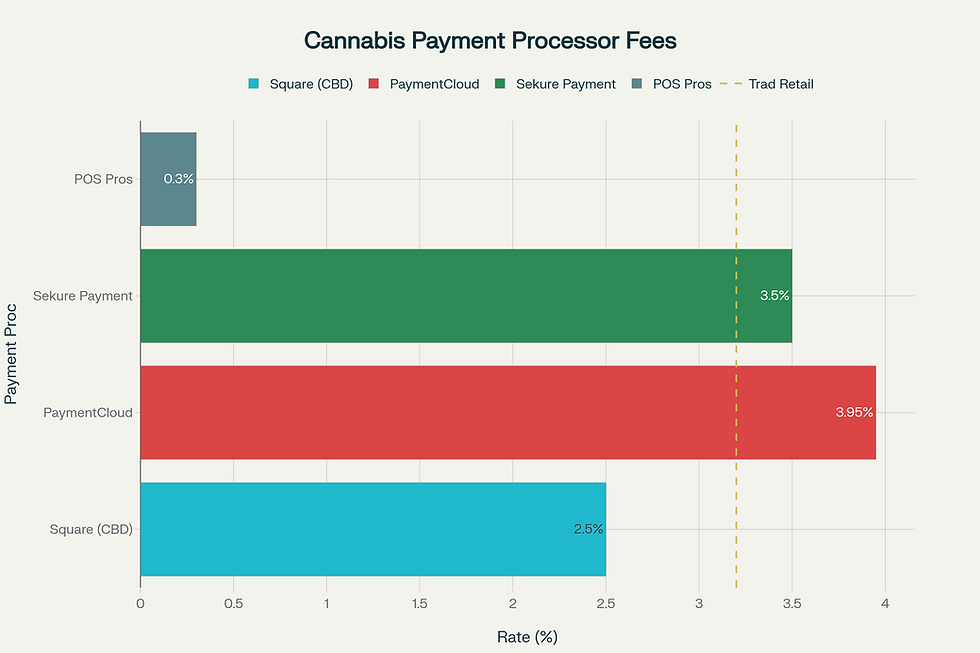

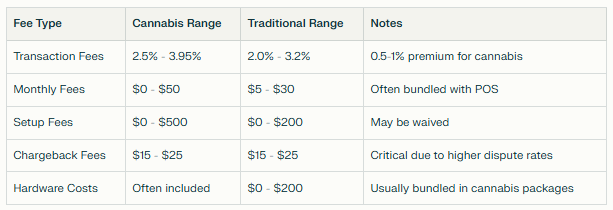

Cannabis businesses typically face transaction fees ranging from 2.5% to 3.95%, significantly higher than traditional retail rates of 2.0-3.2%. Despite these challenges, the industry is expected to reach $45 billion in revenue in 2025, driving continued innovation in payment solutions.

Selection Recommendations

For New Cannabis Businesses

Best bets: Choose Cova Pay or Flowhub for full-service dispensary operations

What should I Budget? 3.5-4% of gross revenue for payment processing costs

Prioritize compliance over lowest fees to avoid regulatory issues. Regulatory/Insurance issues will cost much more than the small extra cost in your monthly operational budgets. We've seen it many times within the Cannabis industry and industry verticals outside of it.

Low-dose THC/CBD... Do not start with Square for CBD-only operations under 0.3% THC. North offers payments at 2.69% (no per-transaction fee) or lower. They approve with the merchants the business before you start taking payments, so any issues are minimal. When they arise, Carpfish advisors or our broker network fixes them quickly.

For Established Dispensaries

Evaluate current processor performance annually as part of your process.

Negotiate better rates based on transaction volume and processing history as a business progresses. Long-term payment contracts aren't usually your friends in cannabis, unlike other industries.

Consider integrated POS solutions for operational efficiency. How much time do you spend on uploading, double-entry, and lazy mistakes? Create a little chart and track it for a week, and most will be amazed. Process efficiency kills margins.

Diversify payment methods to r

For Established Dispensaries

Evaluate current processor performance annually as part of your process.

Negotiate better rates based on transaction volume and processing history as a business progresses. Long-term payment contracts aren't usually your friends in cannabis, unlike other industries.

Consider integrated POS solutions for operational efficiency. How much time do you spend on uploading, double-entry, and lazy mistakes? Create a little chart and track it for a week, and most will be amazed. Process efficiency kills margins.

Diversify payment methods to reduce customer friction and processing costs. What happens if your cannabis payments go down? Do you have a digital wallet service as a failsafe backup to continue business?

For Multi-Location Operations

Seek processors with multi-state experience

Implement centralized reporting and compliance monitoring

Negotiate enterprise-level pricing and support

Plan for varying state regulatory requirements

Cost Optimization Strategies

Businesses can reduce payment processing costs through several approaches:

Negotiation: Many processors offer negotiable rates, with some guaranteeing to meet or beat competitor pricing. Leaders Merchant Services, for example, offers rates starting at 0.15% + $0 with negotiable terms.

Volume Discounts: Higher transaction volumes often qualify for better rates, with some processors offering interchange-plus pricing for established businesses processing substantial annual revenue.

Surcharging: Retail dispensaries can pass processing fees directly to customers where legally permitted, helping minimize expenses.

Payment Method Mix: Prioritizing lower-cost options like ACH transfers over higher-fee debit transactions can reduce overall processing costs.

Fee Reduction Techniques

Negotiate Rates: Many processors offer negotiable pricing

Volume Discounts: Higher transaction volumes often qualify for better rates

Bundle Services: Combining POS and payment services can reduce costs

Surcharging: Pass processing fees to customers where legally permitted

Payment Method Mix: Prioritize lower-cost options like ACH transfers

Financial Planning

Monthly Processing Costs: Budget 3-4% of gross revenue for payment processing

Setup Costs: Factor in one-time implementation expenses

Compliance Costs: Include ongoing regulatory and reporting expenses

Reserve Requirements: Some processors require cash reserves for high-risk accounts

Base Selection Criteria for Cannabis Payment Processors

Essential Features

High Approval Rates: Look for processors with 90%+ approval rates

Cannabis Expertise: Industry-specific knowledge and compliance support

Multiple Payment Methods: PIN debit, ACH, and emerging technologies

Transparent Pricing: Clear fee structures without hidden costs

Compliance Support: Automated reporting and regulatory assistance

Red Flags to Avoid

Miscoded Merchant Accounts: Illegal and risky workarounds

Offshore Processing: Limited recourse and compliance issues

Hidden Fees: Processors not transparent about total costs

No Cannabis Experience: Lack of industry-specific expertise

Poor Customer Support: Critical for resolving urgent payment issues

Fee Structure Analysis

Cannabis payment processing fees are significantly elevated due to high-risk classification. High-risk businesses typically pay 0.5% to 1% higher than traditional retail rates, with cannabis processors charging between 3.49% to 3.95% per transaction plus $0.15-$0.25 transaction fees.

The complete fee structure includes:

Transaction Fees: 2.5% - 3.95% (vs. 2.0-3.2% for traditional retail)

Monthly Fees: $0 - $50 (often bundled with POS systems)

Setup Fees: $0 - $500 (frequently waived for established businesses)

Chargeback Fees: $15 - $25 per incident (critical due to higher dispute rates)

Regulatory Compliance Requirements

Federal Compliance

Cannabis businesses must navigate complex federal requirements despite state legalization. FinCEN Guidance (FIN-2014-G001) requires financial institutions to file Suspicious Activity Reports (SARs) and conduct enhanced due diligence when serving cannabis businesses.

Under Section 280E of the tax code, cannabis dispensaries can pay 60% to 80% of their profits in federal taxes due to prohibited business deductions. Only Cost of Goods Sold (COGS) can be deducted, severely limiting tax benefits available to other industries.

Form 8300 must be filed within 15 days for any cash transactions over $10,000, while quarterly estimated tax payments remain mandatory despite banking challenges

FinCEN Guidance (FIN-2014-G001): Financial institutions must file Suspicious Activity Reports (SARs) and conduct enhanced due diligence

Bank Secrecy Act (BSA): Requires anti-money laundering compliance

Section 280E: Cannabis businesses cannot deduct normal business expenses for federal tax purposes

Form 8300: Required for cash transactions over $10,000

Major credit card networks, including Visa, Mastercard, and American Express, which previously prohibited cannabis transactions, forcing businesses to rely on alternative payment methods (All major card networks approved cannabis SIC codes in January 2025, to start exploring

PIN Debit: Allowed through specialized networks with proper compliance

ACH Transfers: Permitted with enhanced due diligence and monitoring

Cashless ATM: Popular but facing increased regulatory scrutiny

Cryptocurrency: Emerging option with Bitcoin acceptance by some processors

A recent federal court ruling confirmed that payment processing contracts with cannabis merchants do not violate the Controlled Substances Act and are therefore enforceable, providing additional legal clarity for the industry.

State-Level Requirements & Compliance

Cannabis payment processors must verify state cannabis licenses and maintain ongoing monitoring for compliance violations in all cases. Each state has different requirements for medical versus recreational cannabis, creating additional complexity for multi-state operations. It's highly recommended to work with an experienced high-risk network.

License Verification: Payment processors must verify state cannabis licenses

Transaction Monitoring: Ongoing monitoring for compliance violations

Reporting Requirements: Regular reporting to state regulatory bodies

Product Restrictions: Different rules for medical vs. recreational cannabis

Market Trends & Innovations Happening

Technology Innovations

The industry is experiencing rapid technological advancement with AI-driven fraud prevention, blockchain solutions for transparency, and enhanced mobile payment integration. These innovations aim to reduce transaction risks while improving customer experience.

Legislative Developments

The SAFE Banking Act remains the most anticipated development, potentially allowing traditional financial institutions to serve cannabis businesses without federal penalties. Cannabis rescheduling from Schedule I could also dramatically change the payment landscape.

Federal legalization could enable credit card processing within months of passage, similar to the Canadian market experience. This would significantly reduce processing costs and increase payment options for cannabis businesses. Big changes are expected from Washington on this topic, digital banking, and others in early 2026, per industry expert insiders.

Technology Developments

AI-Driven Fraud Prevention: Enhanced security protocols, reducing transaction risks

Blockchain Solutions: Emerging transparency and compliance tools

Mobile Payment Integration: Growing compatibility with digital wallets

Integrated POS Systems: Seamless online and in-store processing

Legislative Outlook

SAFE Banking Act: Potential federal legislation to allow traditional banking

Cannabis Rescheduling: Possible federal reclassification from Schedule I

State Expansion: Continued legalization across additional states

International Markets: Learning from the Canadian legalization experience

Futures Outlook

Short-Term Expectations (2025-2026)

Continued growth in cashless payment adoption

Increased competition among payment processors

Enhanced mobile and digital wallet integration

Stricter compliance requirements and monitoring with Federal rescheduling expected in early 2026.

Long-Term Projections (2026-2030)

Potential federal cannabis legalization enabling credit card processing or more competition in the market, to decrease overall fees.

Traditional banks are entering the cannabis payment space, offering white label payment options.

Reduced processing fees due to increased competition

Advanced blockchain and cryptocurrency integration to greatly reduce the overall cost of taking cannabis

Top Cannabis Payment Processing Companies (Market Sample)

Cova Pay serves as the best overall solution for brick-and-mortar dispensaries, offering an integrated retail ecosystem with PIN debit, ACH, and gift card processing. The platform supports over 2,000 dispensaries across North America and has won awards for excellence and innovation.

Flowhub provides comprehensive POS and payment integration for dispensaries, featuring cannabis-specific compliance tools, loyalty programs, and next-day funding. The platform supports over 1,000 dispensaries with seamless point-of-banking and ACH solutions.

Both can be obtained, usually with discounting or a proper rollout setup through our Creative Network. Have needs, lets talk!

Tier 1: The Market Leaders

Cova Pay

Best For: Brick-and-mortar dispensaries with integrated POS needs

Transaction Fees: Not disclosed publicly

Monthly Fee: Included in POS fee

Payment Methods: PIN debit, ACH, gift cards

Funding Speed: 1-3 business days

Key Advantages: Integrated retail ecosystem, award-winning platform

Coverage: Serves 2,000+ dispensaries across North America

Flowhub

Best For: Dispensaries seeking integrated POS and payment solutions

Transaction Fees: Not disclosed

Monthly Fee: N/A

Payment Methods: PIN debit, ACH, point of banking

Funding Speed: Next business day

Key Advantages: Cannabis-specific compliance tools, loyalty programs

Coverage: Over 1,000 dispensaries supported

Tier 2: Specialized Providers

Paybotic

Best For: Large cannabis businesses requiring rapid approval

Transaction Fees: Custom pricing

Monthly Fee: Varies (retainer model available)

Payment Methods: ACH, eCheck, PIN debit

Funding Speed: Varies

Key Advantages: 48-hour approval process, established since 2014

Specialization: Medical and recreational dispensaries, e-commerce

PaymentCloud

Best For: Hard-to-approve cannabis merchants

Transaction Fees: 3.95% + 15¢

Monthly Fee: $14.00

Payment Methods: Wide range, including cryptocurrency

Funding Speed: Next business day

Key Advantages: 98% approval rate, high-risk specialist

Notable Features: Free PCI compliance assistance, hardware options

North Payments (formerly NA Bancorp)

Best For: Online CBD and hemp businesses, select Cannabis

Transaction Fees: 2.69% and up.

Monthly Fee: $0 to $39.9,5, depending on volume.

Payment Methods: Credit/debit cards for selected cannabis, CBD/Hemp

Funding Speed: Same-day payouts, next day

Key Advantage: Online portal for invoices, remote payments, etc.

Built-in compliance: Customized e-commerce plans, no setup fees

Square and other similar formats

Best For: CBD businesses under 0.3% THC only

Transaction Fees: 2.5% + 10¢ low end.

Monthly Fee: $0 or higher, depending on volume.

Payment Methods: PIN debit, ACH, and limited credit card acceptance for CBD

Funding Speed: 1-2 business days

Key Advantages: Transparent pricing, established brand, quick setup

Limitations: Does not accept high-THC cannabis products. Many times, clients' websites or payment systems will be flagged, and it can take up to 30 business days to clear these issues.

Tier 3: Niche Solutions for Cannabis & THC/CBD

Bankcard International Group (BIG)

Best For: Multiple payment method requirements

Transaction Fees: Not disclosed

Monthly Fee: Not disclosed

Payment Methods: PIN debit, ACH, eCheck, Bitcoin

Funding Speed: Next business day

Key Advantages: BBB accredited, comprehensive educational resources

Notable Features: Tokenization and encryption of data

Green Check Direct

Best For: Comprehensive cannabis banking solutions

Transaction Fees: Not disclosed

Monthly Fee: N/A

Payment Methods: ACH, PIN debit, wire transfers

Services: Payment processing, banking, business loans, HR solutions

Coverage: Full fintech ecosystem for cannabis businesses

North Payments (formerly NA Bancorp) *Carpfish Preferred Provider

Best For: Online CBD and hemp businesses, select Cannabis

Transaction Fees: 2.69% and up.

Monthly Fee: $0 to $39.9,5, depending on volume.

Payment Methods: Credit/debit cards for selected cannabis, CBD/Hemp

Funding Speed: Same-day payouts, next day

Key Advantage: Online portal for invoices, remote payments, etc.

Built-in compliance: Customized e-commerce plans, no setup fees

Square and other similar formats

Best For: CBD businesses under 0.3% THC only

Transaction Fees: 2.5% + 10¢ low end.

Monthly Fee: $0 or higher, depending on volume.

Payment Methods: PIN debit, ACH, and limited credit card acceptance for CBD

Funding Speed: 1-2 business days

Key Advantages: Transparent pricing, established brand, quick setup

Limitations: Does not accept high-THC cannabis products. Many times clients' websites or payment systems will be flagged, and it can take up to 30 business days to clear these issues.

-----------------------------------------

The cannabis payment processing landscape in 2025 offers more viable options than ever before, though challenges persist due to federal prohibition. Success requires partnering with experienced, compliant processors who understand the unique needs of the cannabis industry while maintaining focus on regulatory compliance and operational efficiency.

To learn more, visit High-Risk Merchant Accounts Simplified

or reach out to us at info@carpfishcreative.com

Comments